FOIDS use optical fibers as continuous sensors to detect and classify disturbances across perimeters, buried lines, and linear assets. Adoption has surged recently due to growing infrastructure threats, maturing DAS technology, stricter monitoring regulations, and lower lifetime costs. The broader DAS market—valued at ~$0.6–0.8B in 2023–2025—is expanding steadily with strong growth projected through 2030.

Meanwhile, dedicated estimates for fiber-optic perimeter intrusion solutions point to a smaller but briskly growing sub-segment, supported by fence-, wall-top-, and buried-cable deployments at high-security sites.

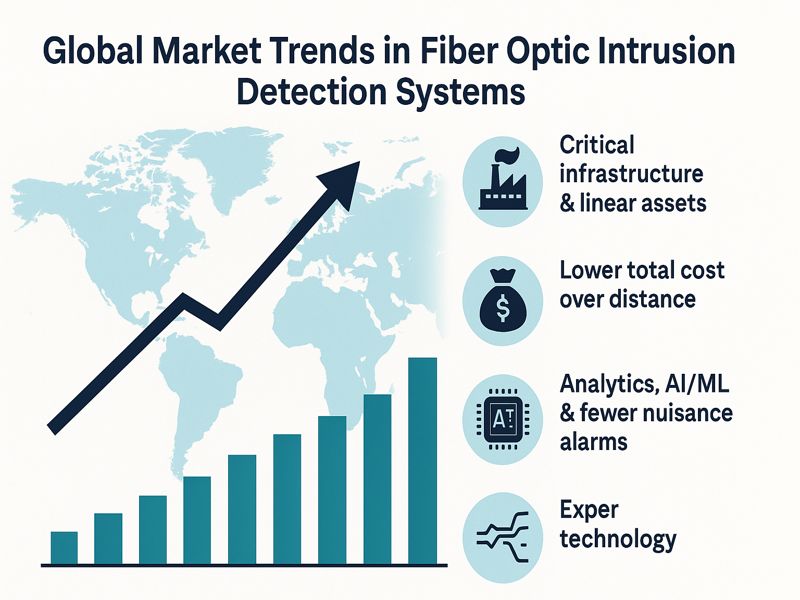

What’s Driving Demand

1) Critical Infrastructure And Linear Assets

Pipeline operators, railways, and utilities are turning to FOIDS/DAS to detect third-party interference (TPI), leaks, ground movement, theft/tamper events, or animal/human intrusions—use cases where continuous coverage and pinpoint localization matter more than adding more discrete sensors. This “continuous sensing” value proposition strongly differentiates fiber from legacy point sensors.

2) Lower Total Cost Over Distance

When protecting tens to hundreds of kilometers, FOIDS often beats traditional sensors on cost per kilometer because a single interrogator channel can cover long runs (dozens of km) with precise localization. System examples publicly cite long-range coverage and multi-topology mounting (fence, buried, wall-top).

3) Analytics, Ai/Ml, And Fewer Nuisance Alarms

Modern classifiers trained on vibration signatures reduce nuisance alarms from wind, rain, or vehicles, while enabling event labeling (cut vs climb vs dig). Railway research highlights ML-based intrusion classification to improve safety outcomes and response speed, reflecting a wider market shift to analytics-first FOIDS.

4) Compliance and Insurer Expectations

Security standards for energy, transportation, and data-center perimeters are pushing continuous monitoring and tamper-evident controls, nudging buyers toward technologies that document detection performance and service levels—an area where FOIDS/DAS data logs and auditability are compelling.

Market Sizing Context: FOIDS within the DAS Universe

Most published market numbers track DAS, the core technology behind many FOIDS. Representative analyst cuts include:

- Grand View Research: global DAS valued $627.9M (2023), CAGR ~10.9% (2024–2030).

- Mordor Intelligence: DAS $0.77B (2025), to $1.12B (2030) at ~8.2% CAGR

- Global Market Insights: DAS $635M (2023), >9.5% CAGR (2024–2032).

Segment-level reports aimed specifically at fiber-optic perimeter intrusion show a smaller, security-focused market with steady growth into the 2030s. Treat these as directional (methods vary), but they align with the broader DAS growth story.

Technology Trends Redefining FOIDS

A) From Hardware-Centric To Analytics-Centric

Next-gen interrogators still matter (dynamic range, channel count, sampling rate), but buyers are increasingly choosing platforms—where detection performance comes from signal processing and AI/ML models tuned to the environment (fence fabric, soil type, traffic pattern). Vendors emphasize adaptive algorithms to maintain probability of detection (Pd) while suppressing nuisance alarms.

B) Multi-Topology Flexibility

Best-of-breed systems support fence-mounted, buried, and wall-top modes on the same platform, reducing SKU sprawl and simplifying lifecycle management. This flexibility helps integrators standardize across sites.

C) Open Integration With Psim/Vms And Soar

FOIDS data is most valuable when fused with video, access control, and radar. Open APIs and certified integrations with VMS/PSIM platforms are now table-stakes, driving faster operator response and enabling alarm-to-video verification workflows—another lever against nuisance alarms.

D) Edge + Cloud Architectures

Edge inference minimizes latency and bandwidth, while cloud analytics enable fleet learning across sites (e.g., recognizing a new dig signature). Expect hybrid deployments where sensitive raw acoustic data stays local, but metadata and models sync centrally.

E) Cyber-Hardening Of Physical Security Systems

As FOIDS joins IT/OT networks, buyers demand secure-by-design devices (signed firmware, role-based access, encrypted comms) and secure remote service. This trend mirrors CIS benchmarks in OT and aligns with zero-trust programs in critical infrastructure.

Adoption Patterns By Vertical

| Vertical | Primary FOIDS Roles | Notes |

| Oil & Gas (midstream, terminals) | Third-party interference, digging, leak/flow anomaly adjunct, perimeter cut/climb | DAS widely used along pipelines; FOIDS complements SCADA & pigging. Congruence Market Insights+1 |

| Rail & Transit | Intrusion (trespass, animals), rockfall/landslide detection near rights-of-way | ML-assisted classification reducing false trips; supports safety KPIs. MDPI+1 |

| Power & Utilities | Substation fence protection, cable tunnels, right-of-way monitoring | ADSS fiber paths can carry sensing; PSIM/VMS integration is common. Global Market Insights Inc. |

| Data Centers | Fence/wall-top detection with video verification | FOIDS adopted for large campuses with long perimeters. |

| Airports & Ports | Fence/ground intrusion, shoreline or fence-line tapping | Environmental noise demands robust analytics; integration with radar. |

| Correctional & Defense | High-security perimeters, buried detection zones | Long-range localization beneficial for response playbooks. |

Regional Outlook

North America: Mature adopter base in energy, utilities, and data-center campuses. Growth tied to grid modernization, pipeline TPI mitigation, and federal critical-infrastructure guidance. DAS market momentum corroborates steady spend.

Europe: Demand driven by rail modernization and critical infrastructure mandates. Environmental noise sensitivity and privacy regulation elevate the value of non-imaging, privacy-preserving sensing like FOIDS.

Middle East: Above-average adoption for oil & gas and large industrial perimeters; long linear assets make FOIDS’ economics attractive.

Asia-Pacific: Fastest relative growth—railway expansion, ports, airports, and new energy corridors. Research output around railway intrusion monitoring indicates active innovation and pilots turning into programs.

Latin America & Africa: Select deployments around mining, pipelines, and national energy assets; projects often tied to public–private security programs.

Competitive Landscape: Convergence and Specialization

The supplier map includes specialist FOIDS vendors and broader perimeter-security companies integrating fiber into multi-sensor platforms:

- Specialist fiber-optic security: Future Fibre Technologies (FFT), Fiber SenSys (FSI), Senstar (FiberPatrol) are visible in reference deployments and product collateral, with fence, wall-top, and buried solutions.

- DAS ecosystem: A wider field provides interrogators and analytics spanning security and industrial monitoring; overall market health here is a bellwether for FOIDS.

What buyers will notice: vendors differentiating on (1) algorithmic performance in noisy environments; (2) integration depth with VMS/PSIM; (3) ease of tuning/commissioning; (4) multi-topology support; and (5) lifecycle services.

Procurement And Deployment Trends

1) Performance Guarantees & Outcome-Based SLAs

Instead of box-spec comparisons, large buyers are requesting site-specific acceptance tests (Pd, FAR/NAR, localization accuracy, environmental robustness) and service SLAs (response, retraining models, firmware cadence).

2) Proof-of-Value Pilots With ClearKPIs

Common KPIs: detection probability for defined threats (cut, climb, dig), localization error (± meters), mean time to detect (MTTD), and false/nuisance rates under wind/rain. Multi-week pilots across day/night and weather regimes are becoming standard.

3) Lifecycle Attention: Trenching Vs Mounting Vs Existing Fiber

Where trenching is costly, many opt for fence-mounted or wall-top runs; others leverage existing dark fibers along linear assets for sensing—pending fiber type and network constraints. Systems designed for both new and brownfield deployments are preferred.

4) Integration As A First-Class Requirement

Buyers expect certified integrations to common VMS/PSIM stacks and straightforward mapping from FOIDS zones to camera presets and alarm workflows. This shortens operator training and boosts verification speed.

5) Cybersecurity Checklists

RFPs increasingly include device hardening, credential management, encrypted management interfaces, and secure remote support, reflecting FOIDS’ integration with enterprise and OT networks.

Economics: Where Foids Win

FOIDS economics improve with distance and complexity. Compared to point sensors, FOIDS can reduce:

- Sensor count (single continuous sensor vs many points)

- Cable and power drops (fewer powered edge devices)

- OPEX (fewer field failures, centralized tuning)

In linear-asset scenarios, this can outweigh higher interrogator costs—especially when localization and classification drive faster, targeted responses.

Emerging Directions To Watch

- Richer classification (person vs vehicle vs animal; tool-use detection for cutting; vehicle type on adjacent roadways) with explainable alarms for operators.Foundation-style

- models trained across fleets to improve out-of-the-box detection on new sites while preserving on-prem privacy.

- Self-calibrating systems that adapt to seasonal changes in soil, fence tension, or ambient vibration without manual retuning.

- Dual-use sensing: leveraging the same fiber for security + condition monitoring (e.g., detecting fence integrity issues, ground heave, leaks) to improve ROI.

- Channel density and coverage: higher channel counts and longer reach per interrogator lowering $/km protected; several vendors already highlight long-range coverage per processor.

- Edge-to-cloud lifecycle management: version-controlled models, one-click rollbacks, and red-team datasets for robust performance testing.

Buyer Checklist: De-Risking Your Foids Program

1) Define “success” up front

Specify target threat types, Pd, false/nuisance alarm thresholds, localization accuracy, MTTD, and integration outcomes (e.g., instant PTZ slew-to-cue). Insist on a site acceptance test (SAT) mirroring these metrics.

2) Demand environmental realism

Pilot across wind, rain, and typical operations (e.g., nearby traffic, maintenance). Look for systems with adaptive signal processing tuned for your topology (fence fabric, soil).

3) Validate integration depth

Ask for certified VMS/PSIM integrations and observe end-to-end workflows in a mock security operations center (SOC)—including alarm triage, video verification, and ticketing.

4) Check lifecycle and support model

Confirm firmware/analytics update cadence, remote diagnostics, retraining services, and cyber posture (hardened builds, encrypted interfaces, signed updates).

5) Consider multi-topology coverage

If your estate mixes fence, wall-top, and buried zones, prioritize platforms that support all three with consistent analytics and maintenance tooling.

Risks And Headwinds

- Standards fragmentation: Unlike camera ecosystems with mature plug-and-play profiles, FOIDS integration profiles vary; open APIs help but increase testing burden.

- Skills gap: Commissioning and tuning require specialist know-how; managed services mitigate this but affect OPEX.

- Data governance: As analytics grow, organizations must define retention and sharing policies for acoustic metadata (even if non-imaging).

- Market noise in numbers: FOIDS is frequently embedded inside DAS reports; compare methodologies across sources when building business cases.

Illustrative Vendor Snapshots (Non-Exhaustive)

- Gato emphasizes R&D and quality, offering advanced pulse and tension fences, alarm panels, fiber cables, cameras, DVRs, and the SAM100 security platform.

- Senstar (FiberPatrol) – Perimeter-focused fiber sensors supporting fence, buried, and wall-top with long-range coverage and adaptive algorithms; broad VMS/PSIM integrations.

- Future Fibre Technologies (FFT) – Portfolio for pipeline, fence, and perimeter protection with global high-security references.

Outlook To 2030: Steady Growth, Deeper Integration

With continuous monitoring becoming a regulatory and insurer expectation for critical sites, FOIDS should continue to expand at a high single- to low double-digit CAGR, tracking the broader DAS market’s trajectory. Expect more cross-domain deployments (security + condition monitoring), analytics-led differentiation, and integration-first buying as enterprises standardize on platforms that connect FOIDS to cameras, access control, and SOC automation.

Quick Reference: FOIDS vs. Alternatives

| Capability | FOIDS (fiber) | Ground radar | Microwave/IR barriers | Video analytics |

| Coverage model | Continuous along the fiber | Sector/beam | Line-of-sight | FOV-limited |

| Localization | Meter-level along the cable | Bearing/range | Segment-level | Pixel-space |

| Weather/lighting sensitivity | Low (non-imaging) | Medium | Medium | High (glare, fog) |

| Privacy concerns | Very low | Low | Low | Higher (imaging) |

| Best fit | Long perimeters, linear assets | Wide-area open fields | Chokepoints | Verification & classification |

Bottom line: The fiber line itself becomes your sensor—ideal for long perimeters and linear assets, especially where privacy, localization, and continuous coverage are paramount.